The markets have been scorching for the previous six months. The tempo of inflation is calming, the Federal Reserve is predicted to taper off its personal tempo of price hikes, know-how shares are booming on the energy of synthetic intelligence, and general, the S&P gave 5 consecutive months of beneficial properties by the tip of July.

However did we simply see a black swan?

Fitch downgraded the US authorities’s credit standing yesterday, from AAA to AA+, saying that the federal authorities’s fiscal scenario is more likely to deteriorate considerably over the subsequent three years, and noting particularly, “frequent political showdowns to scale back debt and last-minute choices erode confidence.” in monetary administration”.

After the announcement, shares plummeted, and now the phrase on everybody’s lips is “debt.” The credit score downgrade is a stark reminder to buyers that the US authorities is carrying greater than $31 trillion in debt. Through the current debt ceiling battle, the White Home warned that inventory markets may crash if the federal government defaulted.

In response to the uncertainty, buyers are in search of safer choices, and defensive shares are getting consideration. Excessive yield distributed shares It seems as a pretty choice, offering a point of safety in opposition to share depreciation by offering a gentle earnings stream.

Towards this backdrop, some Wall Road analysts gave a thumbs as much as a few dividend shares yielding 12%. to open TipRanks databaseWe sifted by the main points behind these two to seek out out what makes them such compelling buys.

Dynex Capital (DX)

The primary is Dynex Capital, an actual property funding fund (REIT) targeted on mortgages and securities. The Firm invests in these belongings on a leveraged foundation, placing its assets into each company and non-agency mortgage-backed securities, in addition to business mortgage-backed securities. Dynex additionally maintains a spread of “legacy” investments in its portfolio, the single-family, leafy residential and business mortgages from which the corporate originated throughout the Nineties.

Dynex follows just a few easy guidelines in managing its portfolio, utilizing a mix of disciplined capital allocation and complete danger administration to generate long-term whole returns with a wholesome dividend part. As a REIT, regulatory authorities require Dynex to return earnings on to shareholders, and a dividend is a handy method to comply.

The dividend is paid month-to-month, on the present price of 13 cents, or 39 cents per quarter. The final July dividend fee was despatched out on August 1; The annual price of $1.56 provides a strong yield of 12%.

Dynex backs its earnings with deep pockets and loads of liquidity. The corporate ended the second quarter of ’23 with greater than $561.5 million in money and equal liquid belongings, and noticed its guide worth for the quarter improve by 40 cents, to $14.20 per share. Within the curiosity of buyers, Dynex generated a complete financial return of 79 cents per share.

Among the many bulls is Jones Analysis analyst Matthew Erdner who sees match to price Dynex shares as Purchase, with a worth goal of $14. Primarily based on the present dividend yield and projected worth estimate, the inventory has roughly 21% of the overall yield potential.

Erdner’s feedback help his place. He writes of the inventory, “DX continues to commerce at a reduction to reservation and is affordable in comparison with its company friends. We consider DX will commerce near its company friends as capital is deployed at wider spreads and better coupons. Realized hedge beneficial properties, amortization of which is topic earnings tax, supportive of the dividend in 2023 and past, whilst stress stays on internet curiosity earnings (NII) and conventional EAD measures because of increased financing prices.”

Turning now to the remainder of the Road, different analysts additionally like what they see. Designated 3 Buys and no Holds or Sells within the final 3 months, the consensus ranking on DX is a Robust Purchase. Shares are priced at $12.85 and the typical worth goal of $14.33 suggests it should achieve 11.5% heading into subsequent yr. (be seen DX stock forecast)

actual property financing chicago atlantic (to reject)

The second inventory on our listing is one other REIT — however with a “twist,” a sure area of interest that deserves a better look. Particularly, Chicago Atlantic is the mortgage lender of selection for the booming hashish sector in the USA. This isn’t a easy area of interest to occupy. Though hashish is authorized for medical or leisure use in 38 states, it stays an unlawful managed substance below federal legislation, a standing that places limits on Chicago Atlantic’s cross-state operations.

The corporate adapts to this by rigorously analyzing the regulatory obstacles to the hashish business, streamlining its operations to keep up compliance with varied state legal guidelines and improve effectivity. Chicago Atlantic’s mortgage portfolio, as of the tip of the primary quarter of this yr, contained commitments of $328.1 million in financing, throughout 24 corporations. This whole consists of $313.9 million in present loans and $14.2 million in future financing. Of the overall, 88% bear a variable rate of interest.

That portfolio generated $14.9 million in top-tier income throughout the first quarter, a complete that was up 51% year-over-year and beat expectations by $476,000. The underside line, earnings per share of 60 cents per share, was 9 cents higher than anticipated. The corporate will report its second-quarter 23 outcomes on August 9, and analysts count on to see a 54-cent GAAP achieve based mostly on whole income of $15.08 million.

Chicago Atlantic lately introduced a typical inventory dividend fee on June 16 for the second quarter of the yr, which is of explicit curiosity to dividend buyers. Cost was made on June 30, on the price of 47 cents per widespread share; At this price, the dividend each year quantities to $1.88 per share and provides a ahead yield of 12.5%.

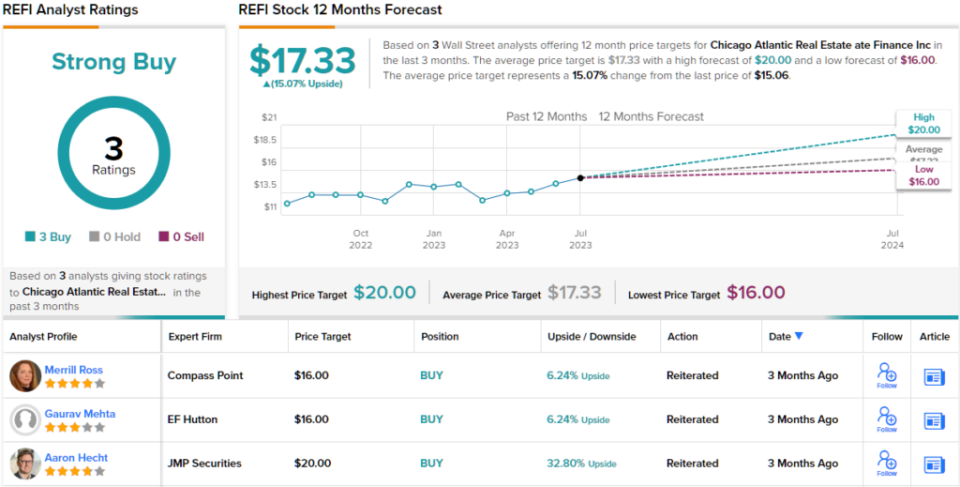

The general high quality of this distinctive REIT has caught the attention of JMP analyst Aaron Hecht, who sees it as a strong choice for buyers trying to ‘get in’ within the increasing hashish business.

The hashish business has felt headwinds related to stagnant federal regulation, low plant costs, and restricted entry to capital. Nonetheless, we consider that REFI’s increased underwriting requirements, which give attention to native market dynamics, money flows and asset protection, materially enhance its danger profile. Hecht writes that REFI can also be the one remaining hashish mortgage fund obtainable within the public markets within the US… We consider capital markets availability will enhance over time, and we stay consumers of REFI.

Wanting forward, Hecht provides REFI inventory an outperform (i.e. Purchase) ranking, with a worth goal of $20 indicating a one-year upside potential of 32%. (To view Hecht’s log, click here)

General, REFI has a Robust Purchase consensus ranking from Road analysts, which is a unanimous sentiment, as evidenced by the three optimistic analyst rankings on report for the inventory. The REFI is promoting for $15.06, and the typical worth goal of $17.33 signifies that there’s a one-year achieve of 15% forward. (be seen REFI stock outlook)

To search out good concepts for dividend shares buying and selling at enticing valuations, go to TipRanks’ Best stocks to buya instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather vital to do your personal evaluation earlier than making any funding.