font dimension

Apple shares are up 50% up to now this 12 months.

Victor J. Blue/Bloomberg

apple

‘s

The June quarter’s earnings report would not be a lot of a development story, and with the inventory already up 50% for the 12 months up to now, there’s not a lot room for error.

However the firm’s bullish group of analysts is predicting higher development forward, predicting extra beneficial properties for what’s already essentially the most useful firm on the planet, with a market cap of $3.1 trillion.

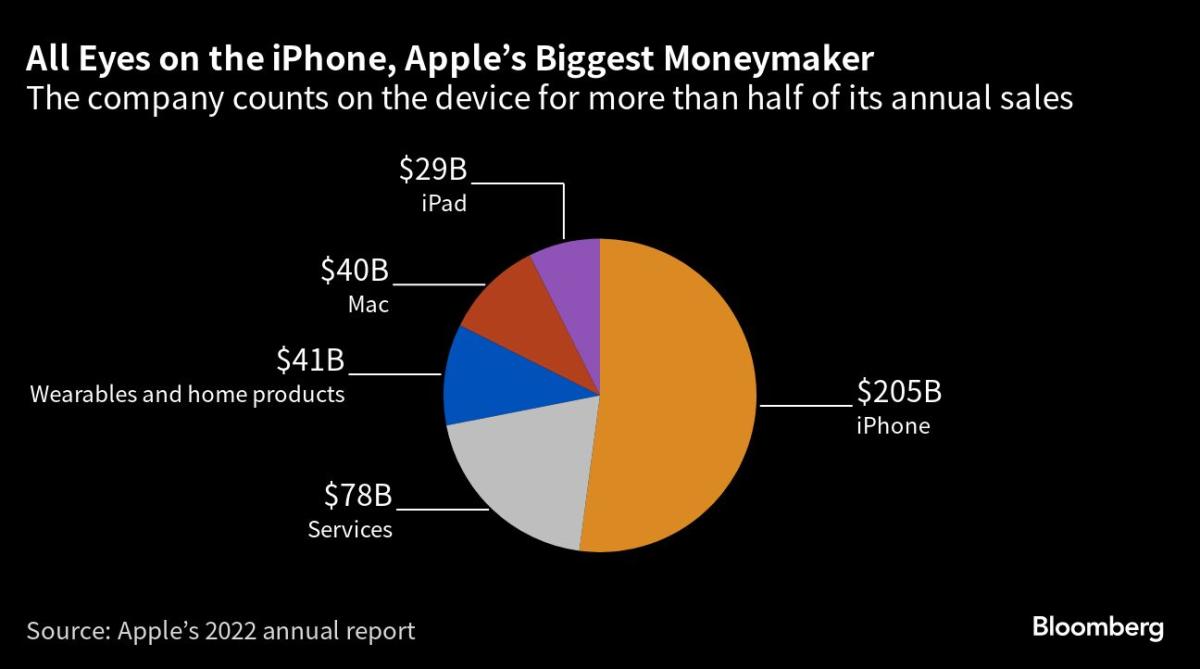

Apple (Inventory ticker: AAPL) will problem a report after the shut of buying and selling on Thursday. For the third fiscal quarter, analysts count on gross sales of $81.9 billion, down about 1% from the year-earlier quarter, with earnings of $1.19 per share, down a penny from a 12 months in the past.

The Road sees iPhone gross sales of $40.3 billion, which is able to drop about 1%, in keeping with FactSet, with Mac gross sales of $6.6 billion and iPad gross sales of $6.5 billion, each down about 10%. These declines are anticipated to be offset by the “wearable, house and equipment” class, with estimated gross sales of $8.3 billion, a rise of three%, and companies revenues of $20.8 billion, a rise of 6%.

One of many keys to this quarter might be what Apple does within the “Better China” class, which incorporates the mainland in addition to Taiwan, Hong Kong, and Macau. Road estimates income is $13.6 billion, which might be down 7%. Income from the Americas is anticipated to be $38 billion, up 1.5% from the earlier 12 months.

Within the third-quarter outcomes report for the month of March, said Apple Chief Financial Officer Luca Maestri Income efficiency in June might be much like the March quarter, which was down 2.5% from a 12 months earlier. Maestri mentioned on the time that the forex would cut back income by about 4 proportion factors, and the companies enterprise would proceed to face macroeconomic headwinds in digital promoting and video games.

Discover the digital promoting exercise in each quarter

the alphabet

(GOOGL) f

Meta platforms

(META) topped Road estimates, which could possibly be a optimistic issue. A secure greenback might imply much less of an affect on the forex than Maestri anticipated.

“China’s telephone considerations about Apple are a bit overblown,” Piper Sandler analyst Harsh Kumar wrote in a analysis be aware reviewing the quarter. He believes the corporate’s earnings name might be properly obtained, pushed by resilience from the China and iPhone segments. On Monday, Kumar reiterated his chubby evaluation, whereas elevating his value goal from $180 to $220.

Dan Ives, an analyst at Wedbush, believes Apple ought to report no less than one quarter of iPhone income, and presumably higher, given the “clear improve in demand across the mainland China area this quarter” for iPhones.

Write to Eric J. Savitz at [email protected]